Why Shield Plan Expenses Matter in Retirement—and How to Present It with Edge

In today’s evolving healthcare landscape, one area that often goes overlooked in financial planning conversations is Shield Plan expense planning—especially for retirement years.

With rising awareness of premium hikes across both MediShield Life and private Integrated Shield Plans, clients are starting to ask more questions. But many still lack a clear framework for understanding what it means for their long-term financial well-being.

That’s where you, the consultant, step in—and where Edge becomes a powerful tool.

Why Shield Plan Costs Deserve a Dedicated Discussion

Over the years, we’ve seen premiums rise sharply—particularly for older age bands. These increases are no longer theoretical; they’re reported across mainstream media and experienced by clients themselves.

As healthcare costs continue to rise and underwriting gets tighter with age, Shield Plan premiums are becoming a material line item in retirement budgeting.

If ignored, they can quietly erode a client’s retirement drawdown plan. If addressed early, they become a manageable, planned-for expense that safeguards health and lifestyle.

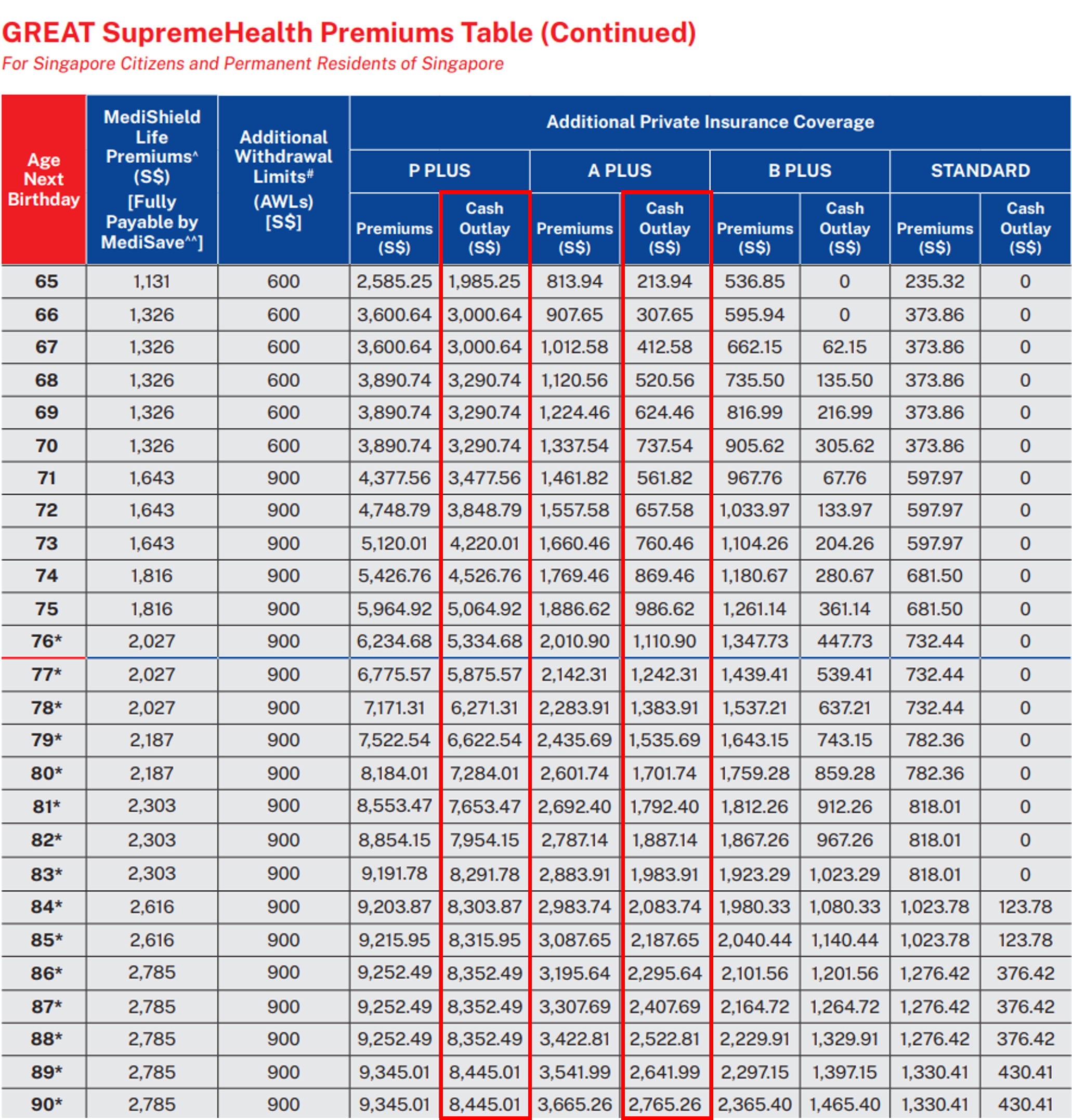

Total Cost Projection: Great Eastern Shield Plan Case

We’ll use the Great Eastern Shield Plan premium table as a reference to illustrate the current potential cost of Shield Plans. Following that, we’ll walk through a roleplay scenario demonstrating how Edge can effectively highlight the urgency of planning for these expenses.

We’ll examine the cash outlay required for both private and Government A1 Shield Plan options, covering both base plan and rider components. From there, we’ll work through an estimated calculation that consultants can use to implement this planning within Edge.

Base Plan Table

Total Cash Outlay for P Plus (65 to 85) - $110,904

Total Cash Outlay for A Plus (65 to 85) - $23,562

Riders Table

Total Cash Outlay for P Signature (65 to 85) - $217,629

Total Cash Outlay for P Optimum (65 to 85) - $65,345

Total Cash Outlay for A (65 to 85) - $37,830

In total, the estimated cash outlay for both the base plan and rider over a 20-year retirement period—from age 65 to 85—is as follows:

P Plus + P Signature - $328,533

P Plus + P Optimum - $176,249

A Plus + A - $61,392

Sample Conversation Flow: Introducing Shield Plan Cost Planning

Previously, we approached this by bouncing the question back to the prospect. Opening the Conversation: How Consultants Can Confidently Introduce Edge in Appointments — A-Think Lab

Here's an alternative way to steer the conversation more proactively:

Consultant: "There’s a ‘silent killer’ that’s quietly affecting many people’s retirement plans these days. Want to take a guess what it is?"

Client: "Inflation?" or "I’m not sure."

Consultant: "Close! It's actually hospital insurance premiums. With an ageing population, higher claim rates, and medical inflation in Singapore around 10%, you’ve probably seen articles about rising premiums—even MediShield Life has gone up."

Client: "Yeah, I think I came across that recently."

Consultant: "Want to guess the total cost someone might pay for hospital premiums from age 65 to 85 if they choose an A Ward/Private Lite/Private plan? (Up to Consultant)"

Client: "Don’t know / Maybe... $30,000?"

Consultant: "It’s actually closer to $61,000. It might not seem like much when broken into monthly or yearly amounts—but over 20 years, it adds up significantly. And that’s today’s estimate—keep in mind these numbers are likely to rise. Let me show you how that looks."

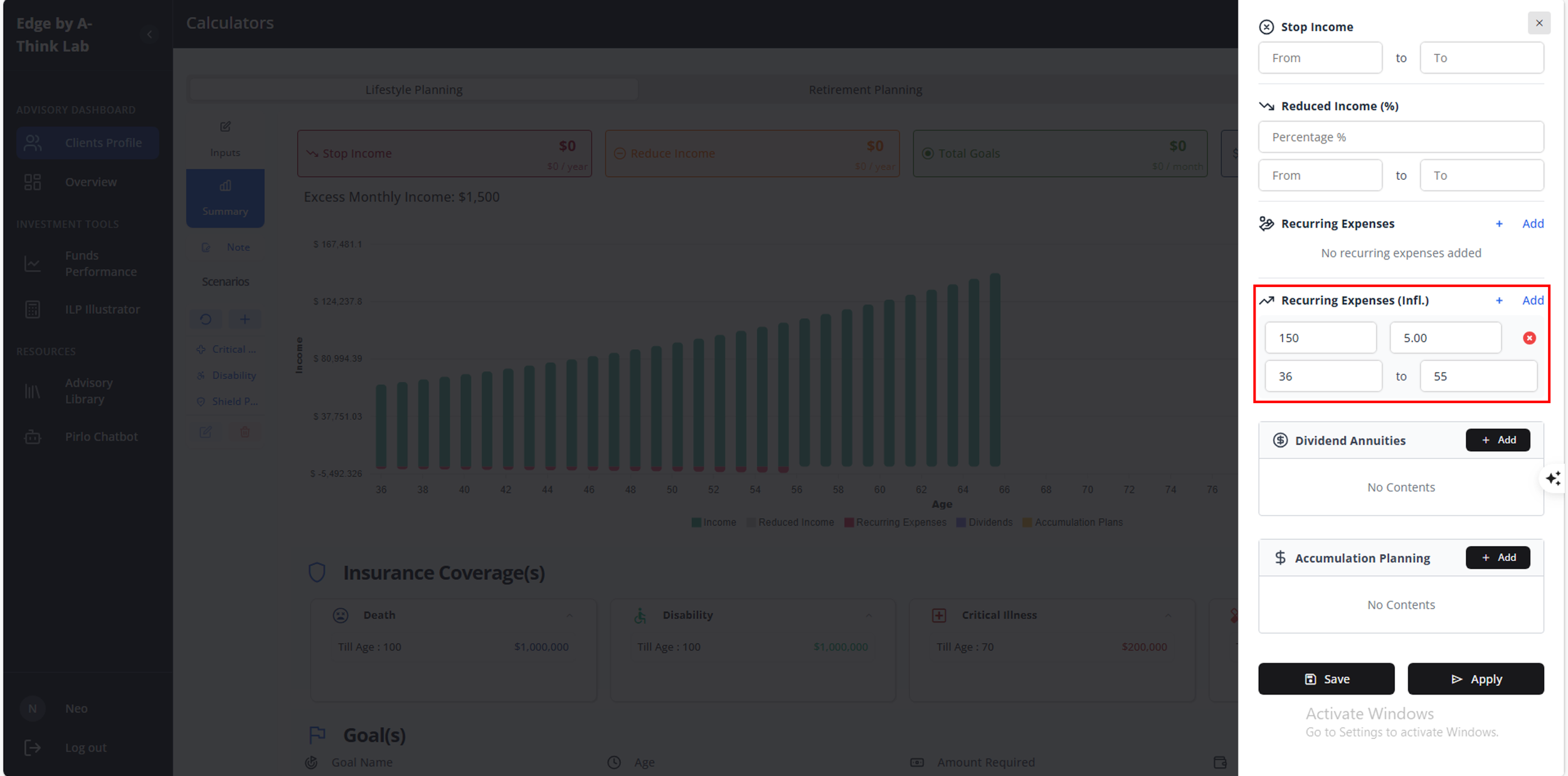

In this example, we use a sample profile of a 35-year-old, projecting Shield Plan expenses from age 36 to 55 to simulate est current 20-year cost breakdown.

This allows the prospect to clearly visualize the potential breakdown and align more easily with your explanation. Consultants can replicate this approach by adjusting the input range based on the profile’s age—for instance, a 40-year-old would use ages 41 to 60.

To closely match the total cost projection from GE, use the following input values:

Private - $800/m & 5%

Private Lite - $420/m & 5%

A Ward - $150/m & 5%

Consultant: "Let’s imagine you’re 65 today—this is how current estimated Shield Plan expenses would progress over time.

It starts at around $1k plus annually, gradually increasing to over $3,000, and totaling est $62,000 by age 85. And that’s assuming you live until 85. If your lifespan extends beyond that, these costs would be even higher."

Client:"Ah, I see what you mean now."

Consultant: "Ok—now let’s fast forward to when you’re 65. Let’s take a look at what those numbers might actually look like for you."

Just update the age range to 65 to 85, and the revised impact will be automatically reflected

Consultant: "Take a look—the total projected amount could grow to nearly $277,000 for your profile, based on a conservative 5% annual increase."

Client: "Wow, that’s a lot. Maybe I’ll just cancel my hospital plan by then. (Haha)"

Consultant: (chuckles) "Haha, I get the reaction—but hospital plan is really the most important layer of protection. The one thing we can be hopeful about is that our income may grow at a similar pace to help offset this. Still, as your consultant, I feel it’s important to highlight this early—so you can plan ahead and stay ahead."

Client: "So what do you suggest?" (The perfect opening for your proposal.)

The consultant can then guide the client in setting up an accumulation plan to build a dedicated fund for future hospital expenses.

To support this, consultants can refer to the previously shared link, which demonstrates how to use the projected planning tool under Retirement Planning to calculate the savings needed to reach various maturity amounts based on the estimated healthcare costs.